As a small business owner, among your many goals is eventually selling your business and planning for a comfortable retirement. The cash balance plan (CBP) offers an effective retirement savings maximization approach that’s gaining traction among business owners. This plan combines features of both defined benefit and defined contribution plans, creating a unique structure that can benefit both you and your employees.

While CPBs can get complicated, I wrote this article to provide a fundamental overview. My goal is to help small business owners make informed decisions about their retirement savings.

What Is a Cash Balance Plan?

A cash balance plan—also referred to as a hybrid plan—blends elements of a defined benefit plan with a 401(k). It provides an annual account balance for greater transparency, similar to a defined contribution plan, and an assured retirement payout like a defined benefit plan. However, rather than a fixed retirement payout, the benefit is based on the account balance at the time of retirement.

The account grows over time based on the investment results. Upon retirement, plan participants have the option of receiving the entire amount in one lump sum or in installments over time. Typically, these assets are rolled over directly into IRAs upon plan termination.

While CPBs are typically established to aid the owners of a company in maximizing tax-advantaged retirement savings, IRS rules mandate that contributions to a CPB account are to be made on behalf of all eligible employees for the owner(s) to receive their benefits.

Why Are They So Popular?

There are several reasons why cash balance plans have become so popular among small business owners. Let’s take a look at the more outstanding factors:

- Customization: Business owners can tailor the plan to their specific needs and financial capabilities.

- Taxes: Every dollar contributed to the CPB by the business owner, by way of deductions, essentially comes right off the top of the owner’s annual income and thus lowers their marginal tax rate and ultimate tax liability.

- Talent retention: Many small business owners attract and retain top talent by providing employees with a CPB as a component of a competitive retirement strategy.

- Larger contributions: CPBs offer the potential of larger contributions than other popular plans, thereby resulting in improved retirement confidence.

What Are the Downsides to Cash Balance Plans?

These are some of the downsides of CBPs you should consider:

- Required contributions: Even if the amount of benefits is frozen at a future date, contributions are still required for a number of years even if the company is underperforming.

- Owner risks: The investment risks are absorbed exclusively by the business owner.

- Increased guidelines: Nondiscrimination testing is typically required annually.

- Contribution amounts: The amounts of required contributions are subject to change and could go up if the plan’s assets do poorly.

- Cost: The administration cost is typically higher due to premiums, professional service providers, and the need for actuarial services.

Who Is Ideally Suited for a Cash-Balance Plan?

By far, this is the most frequent question I get asked about CPBs.

While CPBs are available to anyone, I’ve found that ideal candidates typically have the following characteristics:

- Owners are older, and most of the staff is younger.

- Owners earn at least $300,000 annually.

- Owners can regularly contribute over $50,000 a year to their retirement goals.

- Companies already provide 3% to 5% of their employees’ income through an employer match, bonus structure, or plan design.

- Companies with strong, consistent cash flow over a minimum 3 to 5-year horizon.

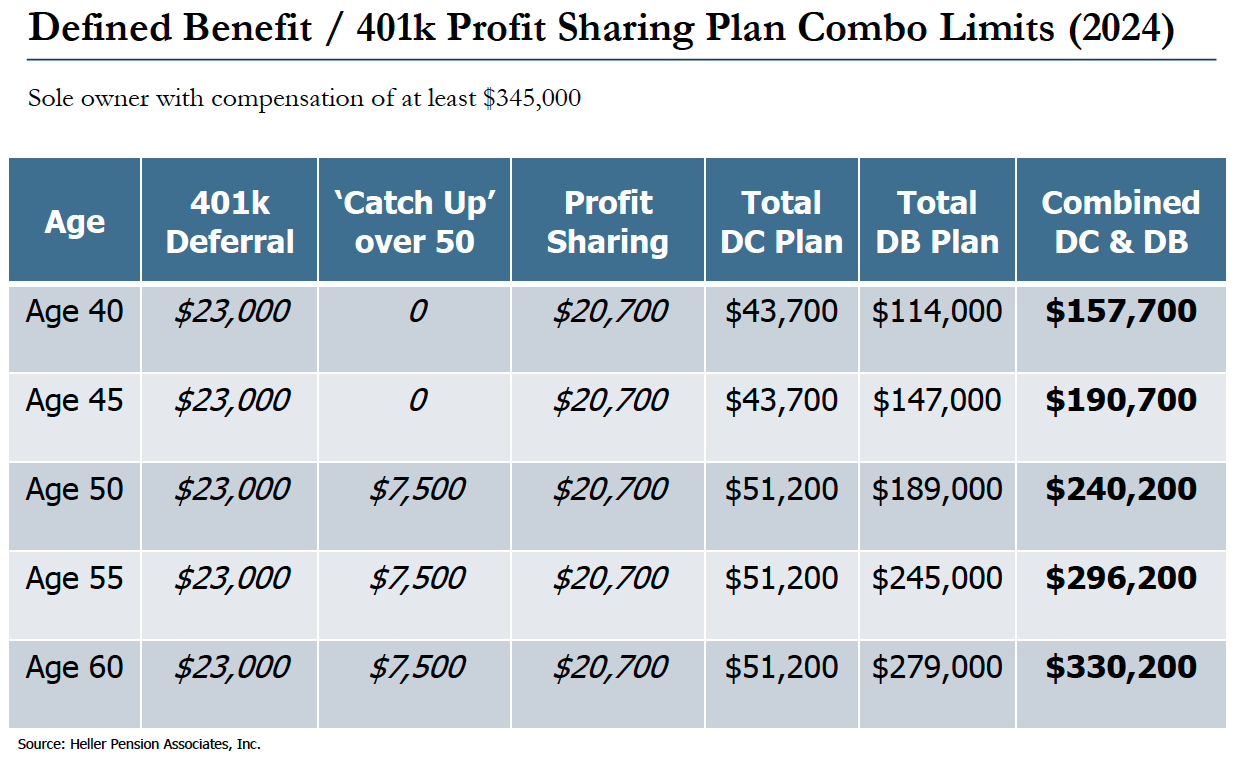

Defined Benefit / 401(k) Profit Sharing Plan Combo Limits (2024)

Sole owner with compensation of at least $345,000

Work With a Professional

Cash balance plans can get tricky. We recommend that you work with a professional financial advisor to help you determine the smartest approach for your business.

At Mendoza Private Wealth, we have 25 years of experience helping small business owners grow and safeguard their wealth with customized retirement plans.

If you’d like help determining if and how CBPs are right for your business, schedule your cash balance plan consultation here.

About Ivan

Iván M. Mendoza is the Managing Principal and a Financial Advisor for Mendoza Private Wealth, a fee-only boutique, private wealth management practice with a focus on research, planning, and investment management. Working with clients in Miami and throughout South Florida, Iván provides investment and wealth planning advice to individuals and families and to their respective trusts, estates, foundations, endowments, and pension plans.

Iván began his career with Prudential in 1999, where he quickly advanced to Manager of Financial Services, overseeing a team of financial planners. In 2012, he joined Sanford C. Bernstein’s private client group as Vice President and Financial Advisor. Driven by his commitment to providing objective advice, he founded Mendoza Private Wealth in 2016. Iván holds multiple designations, including CFA®, CFP®, CDFA®, CLTC®, CLU®, and ChFC®, and is passionate about creating confidence in clients through sound financial planning and investment strategies.

A first-generation American of Peruvian heritage, Iván resides in Miami with his wife, Ana, and their two sons, Emiliano and Alessandro. He enjoys traveling, discovering new restaurants, all things science, World Cup soccer, and staying active through running and biking. An advocate for education, he draws inspiration from his grandfather, a former Minister of Education in Peru, and supports educational causes in his community. Iván is also a music enthusiast with a wide range of tastes, from jazz to reggae to heavy metal. To learn more about Iván, connect with him on LinkedIn.